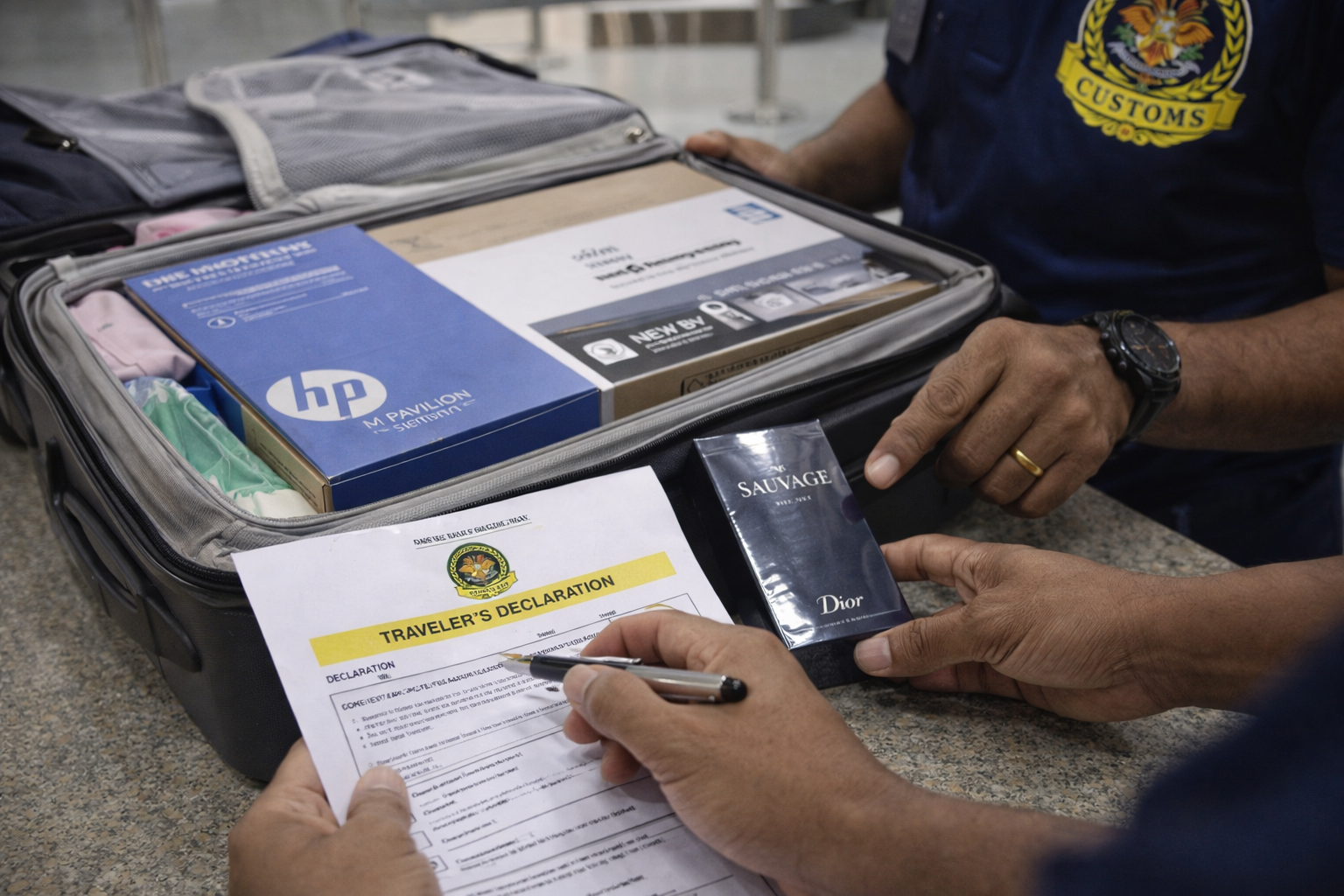

"All travelers are required to declare goods upon arrival, ensuring transparency, compliance, and the proper application of duty-free concessions and taxes."

Duty-Free Concessions & Allowances

Personal Duty-Free Concession (Monetary)

Each traveler receives a monetary allowance for new goods. This does not apply to alcohol or tobacco.

| Adult (18 years and over) | PGK 1,000 |

|---|---|

| Child (under 18 years) | PGK 500 |

Key Rule: Family concessions can be pooled against the total value of the family’s new goods, but a single expensive item cannot be split across multiple allowances.

Specific Item Allowances

Separate from the monetary concession, you may bring limited quantities of the following without paying duty:

- Alcohol: 2.25 litres

- Tobacco: 200 cigarettes or 250 grams of tobacco or 50 cigars

- Perfume: Up to 1 litre

Duty-Free Personal Effects

Calculating Duty & Tax

A Step-by-Step Example

The official example illustrates how a family’s concessions reduce the taxable value of a new item.

Scenario: A family (2 adults, 1 child) imports a new personal computer valued at K5,000. They also have used clothing and camera (duty-free), and alcohol/tobacco within limits (duty-free).

| Calculation Step | Formula | Example Amount (PNG Kina) |

|---|---|---|

| Total Family Concession | K1,000 + K1,000 + K500 | 2,500 |

| Customs Value (CV) | Item Value – Concession | 5,000 – 2,500 = 2,500 |

| Customs Duty (CD) | CV x Duty Rate (e.g., 0% for computers) | 2,500 x 0% = 0 |

| Goods & Services Tax (GST) | (CV + CD) x 10% | (2,500 + 0) x 10% = 250 |

| Total Payable to Customs | CD + GST | 0 + 250 = 250 |

- Customs Value (CV) = Item Value – Passenger Concession

- GST = (CV + Customs Duty) x 10%

- Total Payable = Customs Duty + GST

Rules for Specific Traveler Types

Crew Concessions

Members of aircraft or ship crew on duty are typically entitled to concessions on goods for personal use only, often aligned with the standard traveler allowances. These must be declared upon arrival. Crew may be subject to different clearance procedures.

Commercial Goods

Goods imported for sale, business use, or commercial purposes are NEVER eligible for traveler concessions. They must be:

- Declared separately as a commercial import.

- Supported by a full commercial invoice.

- Cleared by a licensed customs broker.

- Subject to full applicable duties, taxes, and import regulations (which differ from traveler rates).

Compliance, Payment & Penalties

What Happens If I Cannot Pay the Duty?

If you cannot pay the assessed duty and tax on the spot, Customs officials may take one of the following actions:

- Temporary Storage: Place the goods in a secure Customs warehouse at your expense until payment is made.

- Abandonment: You may choose to abandon the goods to the state.

- Security: In some cases, you may be allowed to leave with the goods after providing a suitable guarantee for future payment.

Administrative Penalties

Failure to comply can result in severe penalties under the Customs Act:

- Seizure of Goods: Undeclared goods or goods falsely declared may be seized.

- Monetary Fines: Significant fines can be imposed on the spot or through subsequent legal action.

- Prosecution: Knowingly making a false or misleading declaration (written or oral) is a prosecutable offence under Section 136 of the Customs Act.

Your Responsibilities as a Traveler

- Declare Truthfully: You must accurately declare all goods in your possession on your Incoming Passenger Card.

- Present for Inspection: Present your declaration and goods to a Customs Officer when requested.

- Know the Limits: Be aware of concession limits and understand that exceeding them incurs costs.

- Ask if Unsure: If you are uncertain about an item, always ask a Customs Officer for advice before proceeding.

Disclaimer: This guide is for informational purposes. Concession rates, duty tariffs, and procedures are subject to change under the Customs Tariff Act 1990 and the Customs Act. For authoritative advice, always consult the Papua New Guinea Customs Service directly.

Register for Importing/Exporting

Importing a vehicle

Forms & Guides